The impacts of the COVID-19 crisis on global CO2 emissions and the climate.

The International Energy Agency (IEA) has just published an analysis on the impact of the COVID-19 Crisis. As they predict an unprecedented reduction in energy related CO2 emissions in 2020 the possible impact on the climate could provide completely new arguments for the climate change debate. Here are the key findings:

Global energy and CO2 emissions in 2020

Energy demand

The latest data show that the drastic curtailment of global economic activity and mobility during the first quarter of 2020 pushed down global energy demand by 3.8% relative to the first quarter of 2019. If lockdowns last for many months and recoveries are slow across much of the world, as is increasingly likely, annual energy demand will drop by 6% in 2020, wiping off the last five years of demand growth. Such a decline has not been seen for the past 70 years. If efforts to curb the spread of the virus and restart economies are more successful, the decline in energy demand could be limited to under 4%. However a bumpier restart, disruption to global supply chains, and a second wave of infections in the second part of the year could curtail growth even further.

First quarter of 2020 – compared with first quarter of 2019

Global energy demand in the first quarter of 2020 (Q1 2020) declined by 3.8%, or 150 million tonnes of oil equivalent (Mtoe), relative to the first quarter of 2019, reversing all the energy demand growth of 2019. The drop in global economic activity cut demand for some energy sources much more than for others, with impacts on demand in Q1 2020 going well beyond declines in GDP for certain sectors and fuels.

Coal

In Q1 2020, restrictions on economic activity, as well as changes in weather, hit global coal demand hardest, pushing it down by almost 8% from Q1 2019. The decline took place mainly in the power sector as a result of significant reductions in electricity demand (-2.5%) and competition from very cheap natural gas. The curtailment of industrial production also had an important impact on coal demand over the first three months of the year, with industrial coal demand declining notably in China.

Oil

Global oil demand was down nearly 5%. Restrictions on travel and the closing of workplaces and borders sharply reduced demand for personal vehicle use and air travel, while the curtailment of global economic activity put a brake on fuel oil use for shipping.

Nuclear Power

Output from the world’s nuclear power plants also declined in Q1 2020 as they adjusted to lower electricity demand levels, particularly in Europe and the United States.

Gas

Demand for natural gas declined by around 2% in Q1 2020, with China, Europe and the United States experiencing the most significant declines. The drop in demand in major markets was softened by continued low prices for gas, shifting much of the impact of lower electricity demand onto coal. Gas storage levels rose markedly in Q1 2020 because of increases in year-on-year trade in liquefied natural gas (LNG) combined with lower demand.

Renewable Energy

Renewable energy demand increased by about 1.5% in Q1 2020, lifted by the additional output of new wind and solar projects that were completed over the past year. In most cases, renewables receive priority in the grid and are not asked to adjust their output to match demand, insulating them from the impacts of lower electricity demand. As a result, the share of renewables in the electricity generation mix rose considerably, with record-high hourly shares of variable renewables in Belgium, Italy, Germany, Hungary and eastern parts of the US.

Full Year Projections

The evolution of energy demand through the remainder of 2020 will depend most notably on the duration, stringency and geographical spread of lockdowns, and the speed of recoveries. Initial IEA evaluations indicate that full-year energy demand could decline by around 6%, equivalent to the combined energy demand of France, Germany, Italy and the United Kingdom in 2019. The projected 6% decline would be more than seven times the impact of the 2008 financial crisis on global energy demand, reversing the growth of global energy demand over the last five years. The absolute decline in global energy demand in 2020 is without precedent, and relative declines of this order are without precedent for the last 70 years.

All fuels except renewables are set to experience their greatest contractions in demand for decades. In some cases, annual declines will be stronger than those in the first quarter.

- Oil demandcould drop by 9%, or 9 mb/d on average across the year, returning oil consumption to 2012 levels.

- Coal demand could decline by 8%, in large part due to a fall in electricity demand of nearly 5% over the course of the year, pushing down output from coal-fired generators by more than 10%. The recovery of coal demand for industry and electricity generation in China limits the global decline in coal demand.

- Gas demand across the full year could fall much further than in Q1 2020, because of reduced demand in power and industry applications.

- Nuclear power demand would also fall in response to lower electricity demand.

- Renewables demand is expected to increase because of low operating costs and preferential access to many power systems. Recent growth in capacity, with some new projects coming online in 2020, will also boost output. Biofuels however, are likely to see demand decline, directly impacted by lower transport activity.

Energy demand is set to decline in all major regions in 2020. Demand in China is projected to decline by more than 4%, a reversal from average annual demand growth of nearly 3% between 2010 and 2019. In India, energy demand would decline for the first time, following on from low demand growth in 2019. However, it is advanced economies that will experience the greatest declines in energy demand in 2020. In both the European Union and the United States, demand in 2020 is likely to fall around 10% below 2019 levels, almost double the impact of the global financial crisis.

CO2 emissions

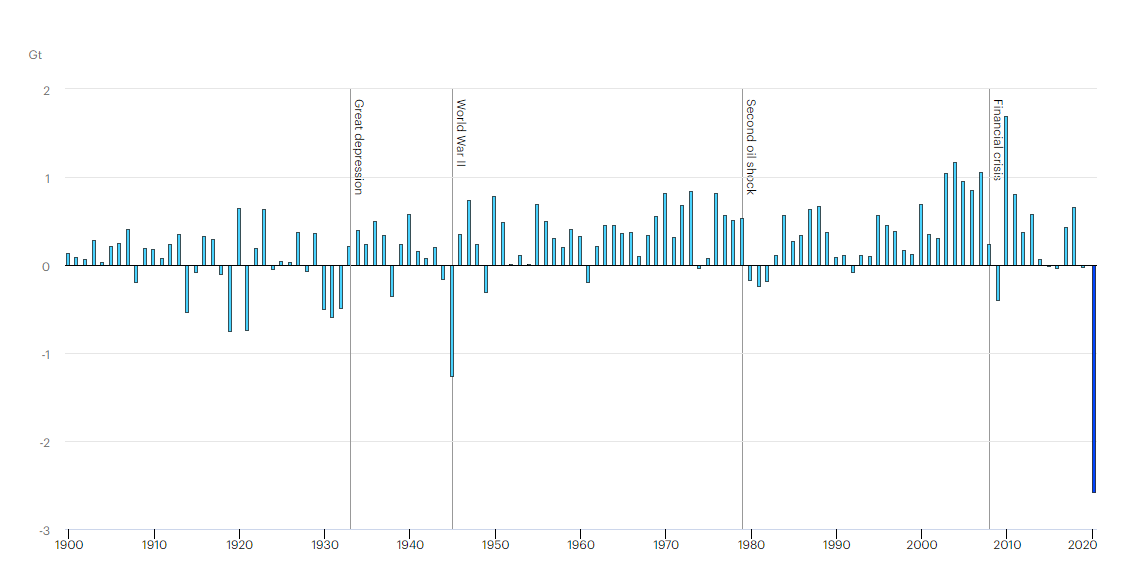

The stunning declines in energy demand in Q1 2020 resulted in a major drop in global CO2 emissions, surpassing any previous declines. Not only are annual emissions in 2020 set to decline at an unprecedented rate, the decline is set to be almost twice as large as all previous declines since the end of World War II combined.

Global CO2 emissions were over 5% lower in Q1 2020 than in Q1 2019, mainly due to a 8% decline in emissions from coal, 4.5% from oil and 2.3% from natural gas. CO2 emissions fell more than energy demand, as the most carbon-intensive fuels experienced the largest declines in demand during Q1 2020.

CO2 emissions declined the most in the regions that suffered the earliest and largest impacts of COVID-19; China (-8%), the European Union (-8%) and the United States (-9%), with milder weather conditions also making an important contribution to the emissions decline in the United States.

Full-year projections

Global CO2 emissions are expected to decline even more rapidly across the remaining nine months of the year, to reach 30.6 Gt for the 2020, almost 8% lower than in 2019. This would be the lowest level since 2010. Such a reduction would be the largest ever, six times larger than the previous record reduction of 0.4 Gt in 2009 due to the financial crisis and twice as large as the combined total of all previous reductions since the end of World War II.

Annual change in global energy-related CO2 emissions, 1900-2020

Of the almost 2.6 Gt reduction in CO2 emissions, reduced coal use would contribute over 1.1 Gt, followed by oil (1 Gt) and gas (0.4 Gt). The United States would undergo the largest absolute declines at around 600 Mt, with China and the European Union not far behind.

Does the reduction of CO2 emissions in 2020 have an impact on the climate?

The question arises whether this is not already a major step towards achieving the Paris climate targets. CO2 emissions could fall back to 2010 levels in just one year! This in turn could lead to the protection of the climate becoming less important. I consider these conclusions to be dangerous and wrong. Nobody can yet predict the reaction of the climate to this short-term CO2 reduction in detail, but there are many indications that the influence on the global mean temperature is within the range of natural variation.The Global Monitoring Laboratory NOAA recently pointed out

If emissions are lower by 25%, then we would expect the monthly mean CO2 for March at Mauna Loa to be lower by about 0.2 ppm. When we look at many years of the difference between February and March we expect March to be higher by 0.74 ppm, but the year-to-year variability (one standard deviation) of the difference is 0.40 ppm. This year the difference is 0.40 ppm, or 0.33 below average, but last year it was 0.52 ppm below average.

Climate change will therefore continue to pose the greatest challenge even after the COVID-19 crisis

Bernd Riebe, May 2020 – IEA (2020), Global Energy Review 2020, IEA, Paris

See also this recent Blue Blog article: Can we see a change in the CO2 record because of COVID-19?

Schreibe einen Kommentar